Executive Summary Equity Market

Global market indices have scaled an all-time high given the ongoing improvement in global and EM growth. Global growth, which in 2016 was the weakest since the global financial crisis at 3.2%, is projected to rise to 3.6% in 2017 and to 3.7% in 2018 (as per IMF projection). Investors have navigated into risk assets since the start of the year leading to appreciation of EM currency and outperformance of EM with respect to DM equities. India too has participated in this rally and has

performed in line with other EM markets.

Q2 FY2018 earnings: After weak Q1 FY2018 earnings season, Q2 FY2018 earnings concluded without any disruption, which witnessed modest improvement in underlying trends in the case of few sectors. Commodities continue to have the lion’s share in terms of their contribution to sales growth. On an aggregate level earnings growth during H1 FY2018 continue to remain subdued with 2% growth. While the base is supportive in H2 FY2018 (Owing to demonetisation), the estimates for earnings growth is still steep (~22%) given the subdued H1 FY2018 results might weigh on full year consensus earnings growth forecast of 12% for FY2018.

We remain cautious with respect to streets estimates of +25% earnings growth for FY2019 earnings given little evidence of a strong turnaround in the demand conditions, which can drive volume growth coupled with high margin and profitability assumptions in several sectors that may be at risk with higher levels of commodity prices coupled with the current slowdown in industrial activity and credit growth. Also, rich valuations of the Indian market make it imperative that earnings do not disappoint, especially in light of the recent increase in crude prices and rising commodity prices leading to input cost pressures.

Improving global environment and robust domestic macro-economic conditions coupled with robust inflows may continue to provide support to equity markets in near term, but we believe earnings will hold the key to market performance in medium to long term given the limited scope of market re-rating. We continue to expect recovery in earnings to be gradual and growth to be moderate than street estimates. We maintain our strategy of staying low beta for the time being.

Valuations remain in expensive zone

- Domestic macros are expected to remain robust: Government measures are expected to drive investment in immediate future. Given the strong domestic fundamentals, we are in the midst of economic uptrend with earnings cycle yet to accelerate to its potential on back of improving utilisation levels and probable pick-up of credit growth.

- Valuations showing stretch – Valuations of Indian equities exhibit stretch. Nifty-50 Index trades at 20.9X FY2018 Expectations and 16.7X FY2019 Expectations (Bloomberg consensus estimates on earnings growth 12% and 25% respectively), leaving very little scope for disappointment in earnings. While the macro story is encouraging and markets may trade at elevated levels in the visible future, valuations pose a risk in the near term.

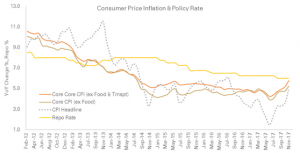

Consumer Price Inflation and Policy Rate

The bigger story in CPI print beyond headline numbers is that the momentum of core inflation accelerated further in November and has now remained elevated for a third straight month. The Core CPI (CPI ex Food and Transport) has printed highest since August 2014, after being stable for 36 months and then rising for last 3 months. This is partly exacerbated by Housing Inflation, given the increase in HRA allowance following 7th Pay Commission. While the HRA momentum may moderate on YoY basis going forward, inflation is expected to continue to follow the RBI projection – averaging 4.7% in Q4 FY2018.

Executive Summary – Debt Market

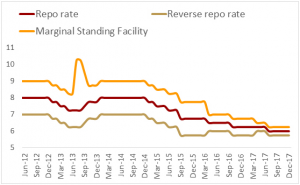

- The RBI kept all rates unchanged in the policy review as was the consensus expectation, while retaining its stance as ‘neutral’

– 5 out of 6 members voted for status quo on rates, one voted for 25 bps rate cut

– Yields were down by 5 bps as hawkishness in tone of RBI was less than what market participants anticipated - RBI has retained the growth forecast at 6.7% for FY2018 despite the Q2 figure falling short of the projection

- RBI has hiked its H2 FY2018 inflation forecast to 4.3% – 4.7% in the second half of the year, rising 10 bps

- The Governor indicated in the call that they will watch incoming information for a quarter or two; thereby implying a long hold. Also, at no point the RBI seemed to indicate possibility of rate hike

- With G-Sec trading more than 100 bps above Repo, which is at higher end of historical average and low probability of hikes in the near future, there is a possibility of spread contraction, all else remaining the same. Hence:

- Prefer hold to duration centric fund and exit on rallies, and

- Continue to prefer shorter tenure portfolios.

Key Policy Rates

Content Source – Content Partner

Checkout various Investment options for NRIs to invest in India